Impact of the Horde Sale

The Daniel Hourdé tribal-art sale is too recent and idiosyncratic, so on its own it does not clearly indicate a broad softening; broader data for 2024–25 actually point to a market that rebounded sharply from 2023 and then normalized rather than collapsed.artmarketstudies+1

Daniel Hourdé sale context

• The Hourdé auction on 25 February 2026 in Paris is a single-owner collection mixing African, Oceanic, Pre Columbian and ancient art plus Hourdé’s own sculpture, so results will reflect the mix of material, estimates, and connoisseurship level of bidders as much as “the market.”sothebysrealty+2

• Such sales often show strong competition for a handful of great, well provenanced pieces and patchier demand for secondary material, which can give the impression of weakness if one looks only at the unsold or low performing lots.sothebysrealty+1

Recent tribal-art market data

• A 2025 report on Africa–Asia–Oceania–Americas arts notes that after turnover fell to a four year low in 2023, the tribal art market “rose to record heights in 2024,” with total global turnover up about 213% year over year to roughly €117.6m, exceeding the previous recent peak in 2021.[artmarketstudies]

• Commentary from specialists in African and Oceanic art stresses that demand has concentrated around high quality, rare works in Paris and New York; this focus on quality has “protected the market” even as other segments of the art world have been more challenged.[theartnewspaper]

How to read current signals

• The broader art market saw a sharp cooling at the very top end (works over 10m USD down more than 40% in 2024), so tribal art is operating in an environment where trophy lot appetite is reduced, but mid market and niche segments can still be healthy.africabasel+1

• Putting this together, recent data suggest: strong recovery in tribal art turnover from 2023 to 2024, continued selectivity with premiums for the best material, and general macro market caution on very high prices, rather than a clear, broad softening specific to tribal art.afrikanizm+2

If you have access to specific Hourdé sale hammer prices versus estimates for key lots, I can walk through them one by one and compare them to earlier benchmark sales to give you a more precise picture.

What’s the main price point you are most worried about (for example, six figure museum quality pieces vs mid five figure good but not masterpiece works)?

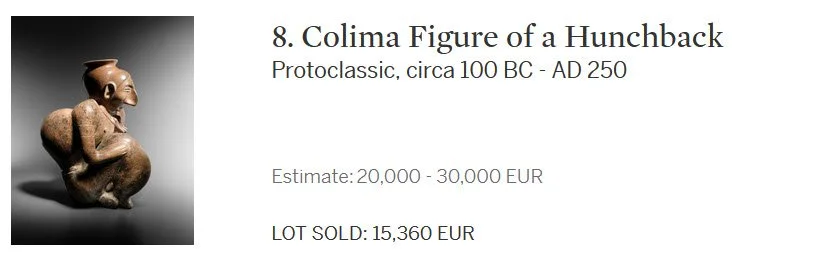

• Colima & Zacatecas (Lots 8, 9) – Pre Columbian figures with good publications or older European provenance have continued to sell well; 20–30k for the Colima hunchback is a “tested” range and not an aggressive estimate for a strong example.

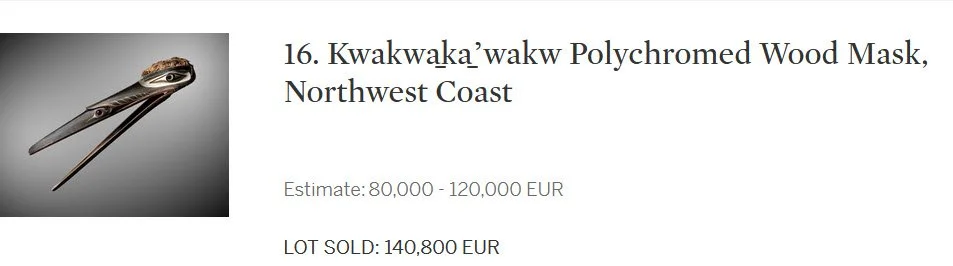

• Northwest Coast & Haida (Lots 16, 29) – Authentic, period Kwakwakaʼwakw masks and Haida frontlets with solid provenance remain highly sought after; estimates of 80–120k and 100–150k are in line with good material from major collections, and when pieces are truly top tier they often exceed this.

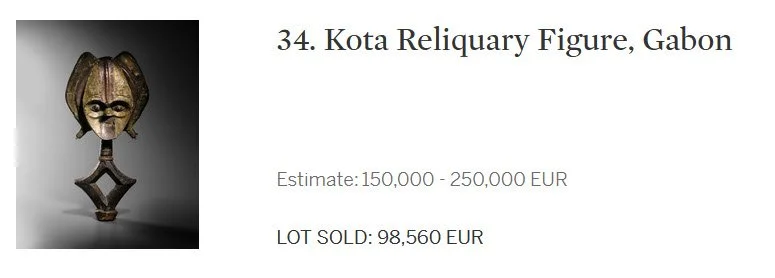

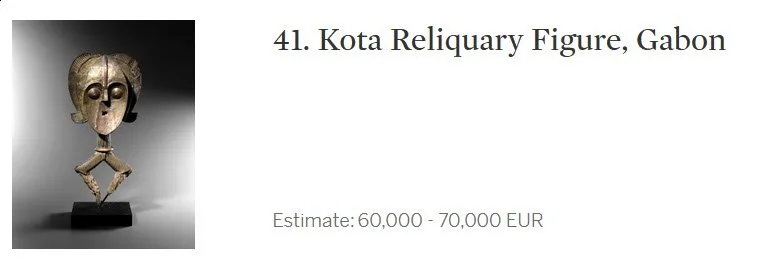

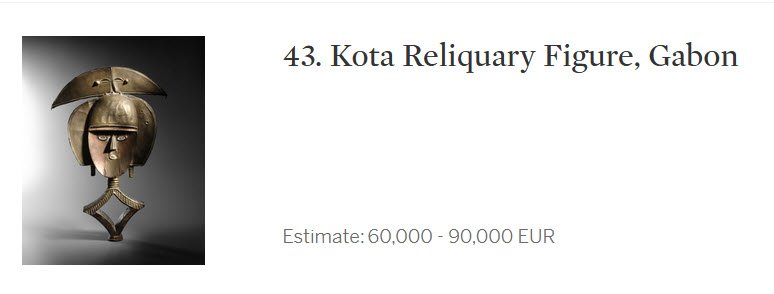

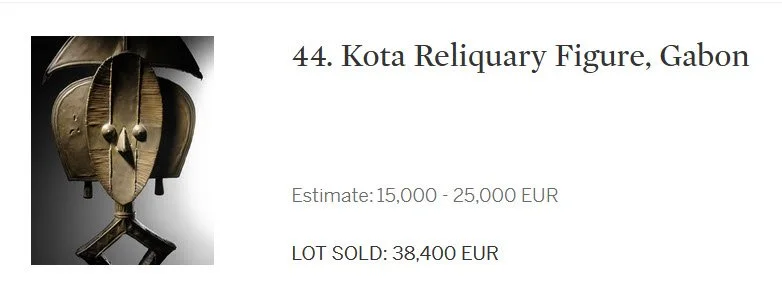

• Top Kota reliquaries (Lot 34) – The 150–250k estimate reflects the very top Kota quality bracket; this is one of the very few African sub categories where prices for exceptional, published examples have proven quite sticky over the last decade.

If these kinds of pieces underperform noticeably (e.g., passed or sold at or below low estimate despite strong quality), that would be a stronger sign of market softening in serious tribal art.

Lots where softness usually appears first

These are still important works but sit in parts of the market that are more sensitive to macro caution and changing taste.

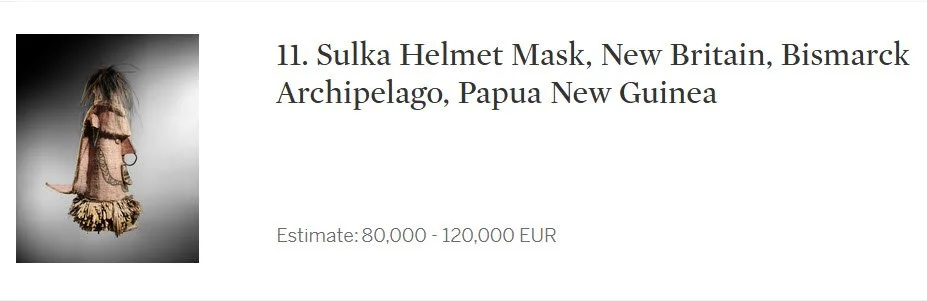

• Sulka, Malagan, Baining–New Ireland group (Lots 11, 12, 14, 15, 22, 23, 25) – Bismarck Archipelago material has a stable but relatively narrow collector base; estimates of 80–120k for the Sulka and Malagan figure are top quartile levels where today’s bidders are very selective about condition, scale, and early provenance. Weak bidding here (selling at low estimate or unsold) would more likely reflect this narrow demand than a collapse of “tribal art” broadly.

• Bembe Gangala statue, DR Congo (Lot 68) – At 60–80k this sits in the mid upper African tier; this is exactly the band that reports flag as most vulnerable to buyers pushing back if works lack exceptional exhibition or publication history.

If you see a pattern across these Oceanic and mid tier African lots of either buy ins or sales only at the bottom of estimate, that is consistent with a soft, very picky market in this band.

Maori and other Oceanic prestige pieces

• Maori prow head and tekoteko (Lots 21, 24) – The 100–150k and 70–100k bands align with serious historic Maori carvings; this is a connoisseur driven niche where fresh to market pieces can still do very well, but “known” examples without exceptional documentation may meet resistance at these levels.

• These results will tell you more about the current appetite of the relatively small circle of Maori/Oceanic specialist buyers than about tribal art as a whole, but a cluster of weak results here would support the thesis that high six figure appetite is thinner outside the absolute top masterpieces.

• Strong outcomes (mid estimate or above) for Lot 34 (Kota), Lot 16/29 (Northwest Coast/Haida) and solid prices for Lot 8/9 (Colima/Zacatecas) would argue against a generalized softening and instead for continued strength for first rate, well provenanced pieces.

• Conversely, if several of the 80–150k Oceanic and Maori lots (11, 12, 16, 21, 24, 29) either go unsold or only clear at or below low estimate, that would support the view that the mid upper tier is softening and buyers are demanding discounts relative to pre 2022 levels, especially for material that is good but not absolutely outstanding.